Tax losses for worthless securities are often challenged by the IRS. It particularly important to document the loss. There are several elements taxpayers have to establish to secure the benefit of tax losses for worthless securities. The recent Giunta v. Commissioner, T.C. Memo. 2018-180, case provides an opportunity to consider these elements. Facts & Procedural History The… Continue reading Documenting Tax Losses for Worthless Securities

Category: Tax Loss

Court Says Partnership is Worth Less, Not Entirely Worthless

The IRS often challenges tax loss deductions. In many cases, it does so by challenging the year in which the loss is allowable. It can be difficult to determine which year the loss should be taken. When an asset is losing value over time, there is a time when the asset is worth less than… Continue reading Court Says Partnership is Worth Less, Not Entirely Worthless

IRS Rejects Court’s Passive Activity Loss 5% Owner and Grouping Decision

The passive activity loss (“PAL”) rules can limit the ability to deduct losses from passive activities, such as rental losses. The real estate professional and activity grouping rules can allow taxpayers to avoid having their losses limited by the PAL rules. Earlier this month, the IRS issued AOD 2017-007, IRB 2017-42 , to note its formal… Continue reading IRS Rejects Court’s Passive Activity Loss 5% Owner and Grouping Decision

Court Says Deduction for Tax Loss Not Allowed for Worthless Debt

Tax losses for worthless debts often trigger IRS audits. On audit, it is common practice for the IRS to disallow the losses based on the debt not being worthless, the amount of the loss not being correct, and that the taxpayer took the loss in the wrong tax year. Taxpayers can take steps to limit… Continue reading Court Says Deduction for Tax Loss Not Allowed for Worthless Debt

Subchapter S Corporation Losses Limited by Tax Basis

One of the benefits of Subchapter S corporations is the ability to have losses flow through from the business’ tax return to the individual shareholder’s tax return. These flow-through losses are limited by the shareholder’s tax basis in the S corporation stock. The court recently addressed this limitation in Tinsley v. Commissioner, T.C. Summary Opinion… Continue reading Subchapter S Corporation Losses Limited by Tax Basis

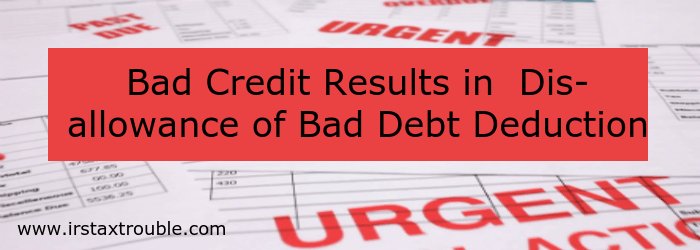

Bad Credit Results in Disallowance of Bad Debt Deduction

The IRS often challenges bad debt deductions–particularly when the loan is from a family member or friend. The courts have developed several factors that they consider in these disputes. One of these factors is whether the borrower would have been able to secure a loan from a third party. The court recently addressed this in… Continue reading Bad Credit Results in Disallowance of Bad Debt Deduction

Bad Debt Deduction for Cease-and-Desist Order

With tax losses, one challenge is to determine what tax year the loss is allowable. The loss year is usually identified by a triggering event. Is a cease-and-desist order from the state regulator a triggering event that establishes that a start-up company is worthless in the year the order was received? The court addressed this in Sensenig… Continue reading Bad Debt Deduction for Cease-and-Desist Order

Grouping Nonpassive Activities Under the PAL Rules

Taxpayers are often surprised to learn that some losses may not be netted against gains in the current tax year. This is often due to the passive activity loss and material participation rules. The IRS National Office addressed these rules in TAM 201634022, in the context of whether two businesses should be grouped together and… Continue reading Grouping Nonpassive Activities Under the PAL Rules

Tax Deductions for Hobby Survives IRS Scrutiny

There are quite a few cases where the IRS disallowed loss deductions for “hobbies.” There are also quite a few cases where the courts have upheld the IRS’s position. These cases are decided based on the facts and how the courts interpret these facts. The facts in Main v. Commissioner, T.C. Memo. 2016-127, provide a… Continue reading Tax Deductions for Hobby Survives IRS Scrutiny

Bad Debt Deduction Not Allowed Until Business Fails

If you lend money to a failing business and the business eventually fails, can you take a bad debt deduction? And if so, when? The U.S. Tax Court addressed this in Cooper v. Commissioner, 143 T.C. 10, which provides an opportunity to consider the question. Facts & Procedural History The Coopers started Pixel in 1983. Pixel… Continue reading Bad Debt Deduction Not Allowed Until Business Fails